Third party risk management has become a cornerstone of operational resilience within the UK financial services sector. As institutions increasingly rely on external vendors, partners, and service providers to deliver critical functions, the ability to manage and mitigate associated risks is paramount. Effective third-party risk management safeguards both financial stability and consumer trust, ensuring institutions can navigate a rapidly evolving landscape.

Current Snapshot: Market Trends and Prevalence:

UK financial services firms are engaging with a growing number of third parties, driven by digital transformation, outsourcing, and the pursuit of cost efficiencies. The sector is witnessing an uptick in partnerships with fintechs, cloud providers, and specialist vendors, reflecting a shift towards more agile and scalable business models. This proliferation of third-party relationships has heightened the need for robust risk management frameworks, as dependency on external entities introduces new vulnerabilities and complexities.

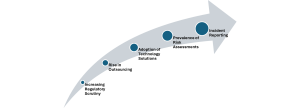

- Increasing Regulatory Scrutiny: Over 80% of UK financial institutions report heightened regulatory requirements around third party risk, driven by FCA and PRA expectations.

- Rise in Outsourcing: Approximately 65% of banks and insurers in the UK outsource key business functions to third parties, including IT, cloud services, and customer support.

- Adoption of Technology Solutions: Around 45% of firms have invested in dedicated third party risk management platforms to automate monitoring and reporting processes.

- Prevalence of Risk Assessments: Nearly 70% of organisations conduct annual risk assessments of their critical third parties, with many moving towards quarterly reviews for high-risk vendors.

- Incident Reporting: In the past year, over 30% of UK financial firms experienced a third party-related incident, prompting increased focus on resilience and contingency planning.

Regulatory Expectations:

The Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) set clear expectations regarding third party risk management. Firms must demonstrate comprehensive oversight of outsourced activities, ensuring contractual arrangements meet regulatory standards for security, continuity, and accountability. Key regulations include the FCA’s SYSC rules, PRA’s outsourcing guidelines, and the UK’s operational resilience framework. Some of the key expectations from the regulators are –

- Regulators such as the Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) expect firms to have robust frameworks in place for identifying, assessing, and managing risks associated with third party relationships.

- Firms must ensure due diligence is conducted prior to engaging with third parties, covering financial stability, operational resilience, data protection, and ethical practices.

- Ongoing monitoring of third parties is required, including regular reviews of service performance, risk exposure, and contract compliance.

- Clear contractual arrangements must be established, outlining responsibilities, reporting requirements, and access rights for regulators.

- Contingency and exit plans should be developed to mitigate potential disruption in the event of third party failure or termination.

- Firms must maintain effective oversight and governance over outsourced activities, ensuring accountability remains with the regulated entity.

- Reporting material outsourcing arrangements to the regulator is mandatory, with prompt notification of significant incidents or breaches.

- Compliance with the FCA’s SYSC rules and PRA’s outsourcing requirements is essential, with a particular emphasis on operational resilience and customer protection.

Current Risks and Challenges:

Third party risk management has become increasingly important for UK financial services, as firms rely more heavily on external vendors and service providers. The complexity of supply chains and regulatory expectations has heightened the need for robust frameworks to identify, assess, and mitigate risks arising from third party relationships.

One of the primary risks is data security and privacy, particularly with the proliferation of cloud services and outsourced IT functions. Financial institutions must ensure that third parties adhere to stringent data protection standards to avoid breaches and regulatory penalties. Additionally, operational risks such as service disruption, cyber-attacks, and dependency on critical suppliers pose significant challenges.

- Cybersecurity Risks: Increased reliance on third parties exposes firms to heightened cyber threats, including data breaches and ransomware attacks. Shared access to sensitive information amplifies the potential impact of a security incident.

- Operational Risks: Outsourcing essential functions can result in loss of control, process failures, or service interruptions, threatening business continuity.

- Reputational Risks: Poor third party performance or unethical practices can damage an institution’s reputation, eroding customer confidence and attracting regulatory scrutiny.

- Compliance Risks: Ensuring third parties adhere to UK regulations, data protection laws, and anti-money laundering requirements remains a persistent challenge, especially with cross-border relationships.

Industry Best Practices:

Third party risk management is a critical aspect of the UK financial services industry, as firms increasingly rely on external vendors, service providers, and partners. Effective risk management safeguards against operational, regulatory, reputational, and cyber risks that may arise from these relationships. The following best practices are widely recognised within the sector:

- Rigorous Due Diligence: Financial institutions conduct comprehensive assessments of potential third parties, evaluating financial stability, security controls, and regulatory compliance.

- Ongoing Monitoring: Continuous oversight of third party activities helps identify emerging risks and performance issues. This includes regular audits, performance reviews, and risk assessments.

- Contractual Controls: Clearly defined contracts establish roles, responsibilities, and service level expectations, including provisions for data security, incident response, and regulatory compliance.

- Collaboration and Transparency: Open communication channels foster collaborative relationships, enabling swift resolution of issues and proactive risk mitigation.

- Incident Response Planning: Ensure response plans are in place to address potential breaches or failures by third parties, including communication protocols and escalation procedures.

- Board Oversight and Governance: Maintain strong oversight by senior management and the board, integrating third party risk into the overall risk management strategy and reporting structure.

- Staff Training and Awareness: Provide regular training to employees on third party risks, contract management, and escalation processes to foster a culture of vigilance and accountability.

The landscape of third-party risk management is poised for further transformation. Advancements in technology, such as artificial intelligence and blockchain, promise to enhance monitoring capabilities and automate due diligence processes. Regulatory developments, including increased scrutiny of critical third-party relationships and tighter operational resilience requirements, will shape future practices. As collaboration models evolve, institutions must remain agile, adapting risk management frameworks to address new threats and opportunities.

Third party risk management in UK financial services is a dynamic discipline, balancing innovation with prudent oversight. Financial professionals and risk managers should prioritise robust risk assessment, diligent monitoring, and transparent collaboration to safeguard their organisations. Staying abreast of regulatory changes and adopting industry best practices will be essential to navigating the complexities of third-party relationships in the years ahead.

Disclaimer :

“The views and opinions expressed by Kavitha in this article are solely her own and do not represent the views of her company or her customers.”

Kavitha Srinivasulu – Senior cyber risk and resilience executive with over 22 years of global leadership experience advising Boards and Executive Committees across Financial Services, Healthcare, Retail, Technology, and regulated industries. Delivered and led large-scale, regulator-driven cybersecurity, AI-driven, PCI, and SOC transformations for Tier-1 banks, global healthcare organisations, and highly regulated enterprises operating across the UK, EU, USA, APAC, and ANZ. Trusted advisor to Boards, C-suite, regulators, and global enterprises, consistently delivering resilient, compliant, and scalable cyber operating models.